Life insurance isn’t just about peace of mind for the future; it can also serve as a lifesaver when you’re looking for ways to secure a loan. This clever maneuver is known as a collateral assignment of life insurance. It’s a deal between you and your lender where your life insurance policy, specifically the cash value component, is used as collateral for a loan.

When assigning your life insurance policy as collateral for a loan, the lender will become a temporary beneficiary of your policy. If the assigner dies before repaying the loan, the lender can claim the death benefit up to the outstanding loan balance. If the policyholder defaults, the cash value of the policy will be collected.

Who can benefit from the collateral assignment of life insurance?

If you need to secure a loan but don’t have typical assets like a house or significant savings, collateral assignment of life insurance could be your ticket. It’s great for small business owners, entrepreneurs, and folks with sizable insurance policies but limited liquid assets.

To use a life insurance policy as collateral, the policy term should be at least as long as the loan duration and should possess a cash value component equal to the loan amount.

What types of life insurance can be used as collateral?

To make this work, you’ll need a permanent life insurance policy that has a cash value component. This includes options like whole life, universal life, and variable life insurance. Unfortunately, term life insurance doesn’t quite make the cut, as it lacks a cash value.

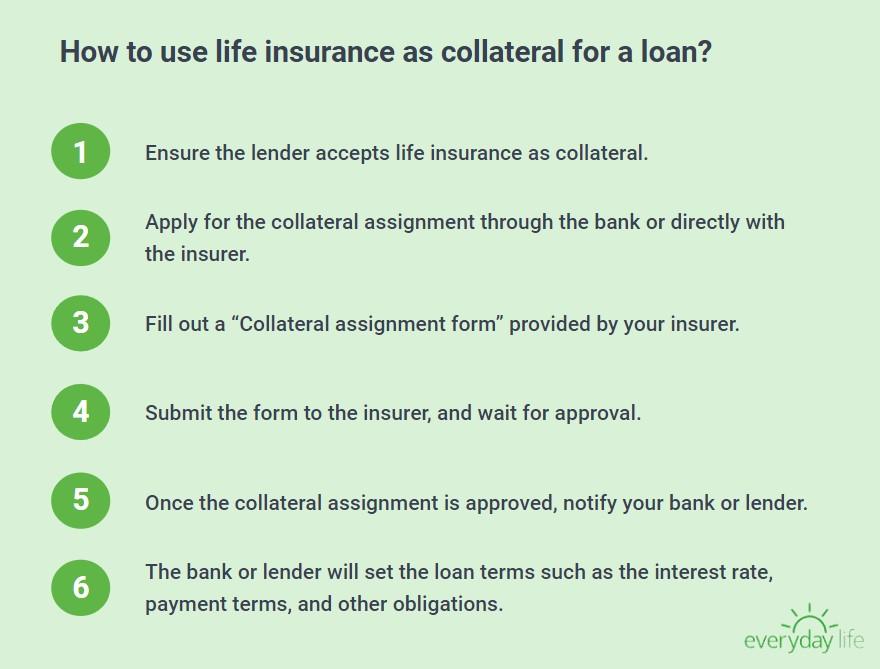

How to use life insurance as collateral for a loan?

1. Ensure the lender accepts life insurance as collateral.

2. Apply for the collateral assignment through the bank or directly with the insurer.

3. Fill out an “assignment of Life Insurance Policy as Collateral form” provided by your insurer.

4. Submit the form to the insurer, and wait for approval.

5. Once the collateral assignment is approved, notify your bank or lender.

6. Bank or lender will set the loan terms such as the interest rate, payment terms, and other obligations.

Is life insurance as collateral widely accepted? Do all banks accept it?

Typically, permanent life insurance policies such as whole life and universal life, which have a cash value component, can be used as collateral. Lenders such as banks want security, and the cash value component of a whole life insurance policy provides this. This cash value grows over time and can be used if the borrower defaults on the loan, which decreases the risk for the lender.

How is the loan amount determined when using life insurance as collateral?

The borrowing capacity is determined as a proportion of the cash value, varying across different insurance companies. Typically, the permissible borrowing range hovers around 90% to 95%. Applying these percentages to a cash value of $50,000, one could potentially secure a loan amounting to $45,000 to $47,500.

What happens when you are unable to pay back the life insurance loan?

The cash value of your policy will be collected by the lender. If this is insufficient, the amount you owe is deducted from the death benefit when you pass away. In some instances, you might also incur a substantial tax bill.

Is the collateral assignment of the life insurance agreement permanent?

No, the collateral assignment of the life insurance agreement is not permanent. It’s tied to the lifespan of the loan. Once the loan is fully repaid, the assignment can be released, and the life insurance policy returns to its original beneficiary arrangement.

What are the tax implications of using life insurance as collateral for a loan?

If the amount you borrow directly from the insurance company is equal to or less than the total insurance premiums you have paid, it is not subject to taxation. However, If you surrender your policy, or allow it to lapse, and the total amount of outstanding loans and interest surpasses what you have paid in premiums, there is a possibility of incurring a tax liability. In essence, you would be required to pay income tax on any investment earnings in that scenario.

Best Online Life Insurance Calculator

At Everyday Life Insurance, we specialize in finding the perfect policy to match your unique circumstances. Whether you’re a small business owner looking to back your loan or a stay-at-home mom working to provide for her family, we’re here to help. Use our online life insurance calculator to find the best plan for your finances, in just 15 minutes.